Let's be honest: you have no idea what your insurance actually covers.

And that's not your fault.

Commercial insurance policies are written by lawyers, for lawyers, about situations lawyers hope never happen. The average policy runs 50–200 pages of nested exclusions, endorsements that contradict each other, and phrases like "occurrence-based coverage trigger" that mean everything and nothing.

$400+

what a broker charges to review one policy

3–5 days

how long that review takes

87%

of business owners who just... guess they're covered*

You're running a business. You don't have time to become an insurance scholar. So you sign the renewal, pay the premium, and hope the coverage gods smile upon you if something goes wrong.

That's not risk management. That's prayer with a deductible.

*We made this stat up. But you nodded, didn't you?

We built this because the status quo kinda stinks.

Traditional policy review has three options:

DIY it.

Clear your weekend. Buy highlighters. Accept that you'll miss something important buried on page 94.

Pay a broker.

$400 per policy. Wait 3–5 days. Receive a PDF that's somehow even more confusing than the original.

Ignore it.

The most popular choice. Also the most expensive—when a claim gets denied because of an exclusion you didn't know existed.

None of these are acceptable in 2026.

We now have AI that can read a 200-page document in seconds, understand context (not just keywords), and explain what it found in language a human can actually parse. So we built the tool we wished existed: fast, cheap, clear, and honest about its limitations.

We read insurance policies so you don't have to.

Here's how.

Step 1

Upload

Drop in your policy PDF. Scanned, digital, coffee-stained—we've seen it all. Up to 200 pages.

Step 2

AI Does the Reading

Our AI doesn't just extract data—it comprehends. It finds endorsements buried on page 83. It catches exclusions that contradict your declarations page.

Step 3

Get Clarity

Plain-English report: what's covered, what's not, what's missing, whether you're getting a good deal, and what questions to ask your broker.

See what you get

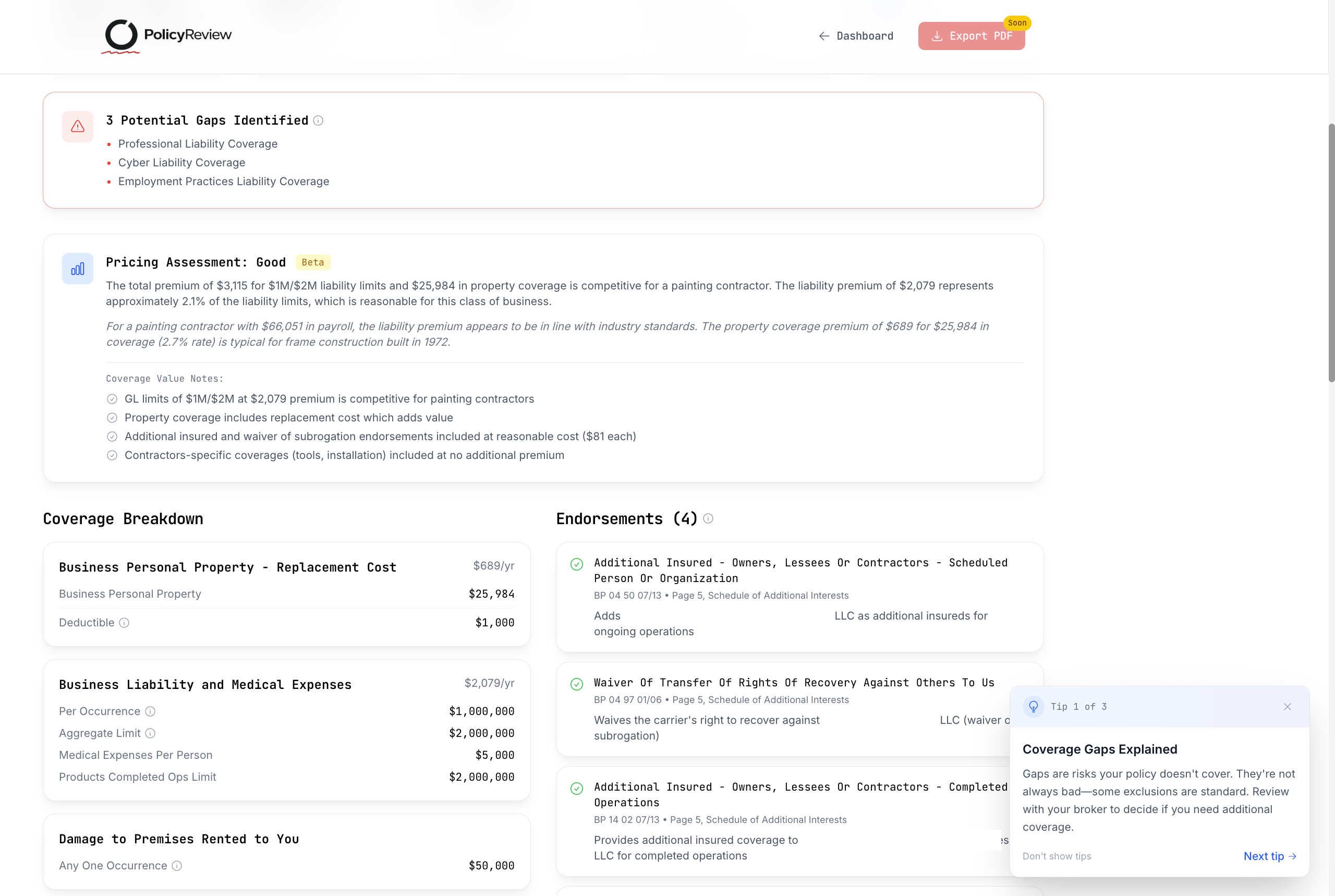

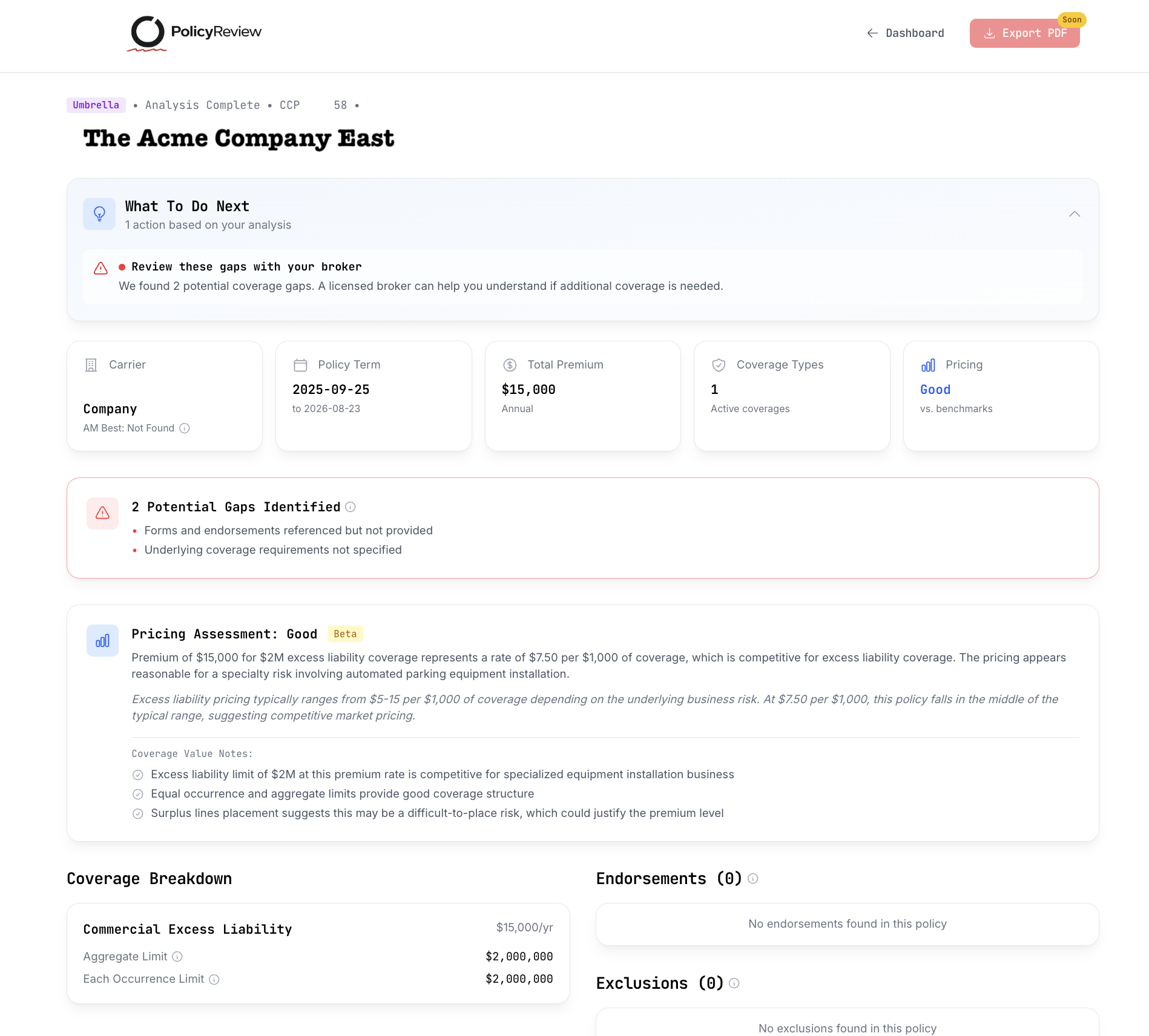

Real examples from actual policy reviews. Gaps identified, pricing assessed, coverage explained.

Gaps, pricing assessment & coverage at a glance

What you'll actually learn

Not a feature list. A "finally, someone told me" list.

"How much am I actually covered for?"

Limits for each coverage type—GL, property, auto, umbrella, WC—in plain numbers

"What's NOT covered?"

Every exclusion, explained in English, with page references

"Did I get those endorsements I asked for?"

Full endorsement list with form numbers and what they actually do

"Are there gaps I should worry about?"

Flagged areas where coverage might be missing or insufficient

"Am I getting a good deal?"

Pricing benchmarks (Beta) help you understand where your premiums stand relative to typical market rates

"Is my carrier financially solid?"

AM Best rating and what it means for your claims

The stuff other tools miss

Most AI policy tools pattern-match. They look for "Limit: $X" in the spots where it usually appears. Ours actually reads.

Endorsements that override exclusions? We catch that.

Coverage buried in a rider on page 147? Found it.

Conflicting language between sections? Flagged with explanation.

We built this for the edge cases—because that's where claims get denied.

"But can I trust an AI with my insurance policy?"

Fair question. Here's our honest answer:

On accuracy:

We're not perfect. No AI is. But we're methodical—our system runs multiple analysis passes, flags low-confidence findings, and tells you exactly where in your policy we found each piece of information. You can verify everything.

On security:

Your policy contains sensitive business data. We encrypt it in transit and at rest. We don't train our AI on your documents. You can delete your data anytime.

On our role:

We're not replacing your broker. We're making sure you don't walk into that conversation blind. Think of us as the friend who reads the contract before you sign it and says, "Hey, did you see this part on page 43?"

The Fine Print (Ours, Not Yours)

This tool points you in the right direction. It does not provide insurance advice, legal counsel, or a guarantee that your next claim won't be a bureaucratic nightmare. Always verify findings with your actual policy. Always consult a licensed professional for coverage decisions. We're a flashlight, not a lawyer.